| "What happens if I forget to pay my SIP installments? Will I be fined?" Click on this link to read the answer. ________________________________________________________________________________________ The English translation is as under:

“Is there any penalty, if I skip an installment or two of my SIP?”

“What is the minimum period for which I must continue my SIP? What

if I don’t? Will my money be confiscated?”

These are some of the questions that I regularly face during my

interactions with investors, especially in large investor meetings. I tried to

understand why these questions keep coming. I think the primary reason is that

SIPs in mutual funds are being compared with other forms of regular savings,

e.g. recurring deposits, insurance premia, PPF contributions. Even EMIs on

loans have various conditions regarding regularity and term.

SIP in a mutual fund scheme, on the other hand is just a convenience

and not a compulsion. At best, it can be termed as a commitment to yourselves.

To that extent, one may start an SIP for 100 years and then discontinue the

same after a few months. While the future installments would not be deposited

in the SIP account, all the previous installments would continue as investments

in the same mutual fund account.

We have discussed in the past about various benefits of SIP. Let us

highlight some of the operational aspects of the same to clarify and answer the

questions raised in the beginning. SIP offers some great operational

conveniences to channel your regular savings into investments of your choice.

The investments can be made in equity funds, balanced funds, debt funds, liquid

funds, international fund or even gold funds – you can choose the option.

You are required to give post-dated cheques or a standing

instruction to your bank through NACH mandate registration. The period can be

chosen based on your cash flow – if you are 55 years and wish to invest for the

next 5 years till your retirement, start an SIP for 5 years. If you are 27

years old and do an SIP for purchasing a house when you turn 33, start an SIP

for 6 years. If you are 31 year old with a 1-year-old daughter, you may start a

16-year SIP to fund her college education.

If you want to increase the amount of SIP, there are few fund houses

that offer you to mention this right at the beginning – you may increase your

monthly investment amount every year by a certain amount. If such option is not

available with the fund house you have chosen, you may always start another SIP

– either in the same scheme or any other scheme. If you wish to change the

scheme, you may discontinue your SIP in the present scheme and start in another

one. All these flexibilities make it convenient for an investor.

Now let us come to the commitment part. What if your cheque bounces?

Not to worry. Most fund houses do not charge any penalty for that. However, in

majority of the cases, if three of your cheques bounce or a certain number of

(three, in many cases) consecutive debits are rejected by your bank (for

whatever reasons), the fund house may consider it as you are not interested in

continuing the SIP and hence stop depositing your cheques or cancel the debit

(NACH) mandate to debit money from your bank account. In case such a thing

happened by mistake, you may always restart an SIP – either in the same account

or in another. There is no revival charge.

At the same time, let us understand the penalty aspect of any

commitment. If you enter into an agreement, and want to terminate the same

before the due date, there could be penalty payable to the other party, as per

the terms of the agreement. As we have already mentioned, an SIP is your

commitment only to yourself and nobody else. This means, if there is any

penalty levied – who would pay and who would get it? The penalty is levied by

your present self and paid by your future self. In other terms, while your

present self may indulge into some spending, the future self is deprived off

wealth and hence purchasing power. This affects the lifestyle of your future

self. Be aware of this penalty. Understand the implication of this. Plan your

SIP keeping in mind your present requirements as well as your future

requirements. Strike a proper balance so that you enjoy life in the present as

well as in the future.

So, please go ahead. Plan an SIP for your future needs, as permitted

by your cash flow.

- Amit Trivedi

|

Thursday, December 29, 2016

What happens if I forget to pay my SIP installments?

Saturday, December 24, 2016

Merry Christmas

Wish you all a Merry Christmas.

The best way to spend time would be to pick up a book. Invest in knowledge. As Benjamin Franklin said, “It pays the best interest”

#RidingTheRollerCoaster

https://ridingtherollercoasterthebook.com/2016/12/24/merry-christmas/

The best way to spend time would be to pick up a book. Invest in knowledge. As Benjamin Franklin said, “It pays the best interest”

#RidingTheRollerCoaster

https://ridingtherollercoasterthebook.com/2016/12/24/merry-christmas/

Ho ho ho, Santa Claus is coming along ...

From the archives:

I wrote this blog roughly five years ago.

Santa Claus Rally

Enjoy while Santa comes along and fulfills your wishes.

I wrote this blog roughly five years ago.

Santa Claus Rally

Enjoy while Santa comes along and fulfills your wishes.

Thursday, December 22, 2016

When bond fund SIP beats equity fund SIP ...

When bond fund SIP beats equity fund SIP…

Investors must understand why such a situation exists and the lessons it leaves for the investors.

Read more at: http://www.moneycontrol.com/news/mf-experts/when-bond-fund-sip-beats-equity-fund-sip%E2%80%A6_8151621.html?utm_source=ref_article

When bond fund SIP beats equity fund SIP: Investors must understand why such a situation exists and the lessons it leaves for the investors.Read more at: http://www.moneycontrol.com/news/mf-experts/when-bond-fund-sip-beats-equity-fund-sip%E2%80%A6_8151621.html?utm_source=ref_article

Investors must understand why such a situation exists and the lessons it leaves for the investors

Read more at: http://www.moneycontrol.com/news/mf-experts/when-bond-fund-sip-beats-equity-fund-sip%E2%80%A6_8151621.html?utm_source=ref_article

Read more at: http://www.moneycontrol.com/news/mf-experts/when-bond-fund-sip-beats-equity-fund-sip%E2%80%A6_8151621.html?utm_source=ref_article

When bond fund SIP beats equity fund SIP…

Monday, December 12, 2016

Chat transcript 12-Dec-2016

Click on the link below to read the transcript of my chat on www.moneycontrol.com today:

http://www.moneycontrol.com/news/mgmtinterviews/chats/detail_new.php?chatid=2775

How do you know which scheme you have invested in?

"How do you know where the mutual fund scheme invests our money?"

To understand the answer to this basic question, click here to read my article in today's Mid-day Gujarati, Mumbai edition.

_________________________________________________________________________________

The English translation is as under:

To understand the answer to this basic question, click here to read my article in today's Mid-day Gujarati, Mumbai edition.

_________________________________________________________________________________

The English translation is as under:

Recently, after an investment seminar, someone approached me and

asked a very basic question: “How do I know if a mutual fund scheme is an

equity fund, a balanced fund, a debt fund or a liquid fund?” Well, for someone

who has spent more than a decade and a half in mutual fund industry, this was

unthinkable. However, the question only reflects that there is still a lot of

work required to spread the awareness about a good investment vehicle.

Well, let us come back to the question that the person asked. How does

one know what type of a fund it is?

A mutual fund is a portfolio of investments. All of us have a

portfolio built by ourselves. We invest some money in bank deposits, some in

company deposits, we buy some debentures, we buy some small savings schemes,

and we also buy some shares or even a real estate property. We refer to a

combination of all these investments together as an investment portfolio.

Similarly, a mutual fund scheme is another portfolio with a few

differences. For one, the portfolio referred earlier is self-managed by the

investor; whereas the mutual fund portfolio is managed by a professional fund

management team. Second difference is huge. While constructing our self-managed

portfolios, we normally do not start with some guidelines regarding how we

would manage the same. In case of a mutual fund, the scheme’s investment

objective, investment style and the investment universe have to be clearly

defined in a legal document called the offer document.

It is this offer document that one must refer to in order to

understand the details of the scheme. Let us introduce this particular

document. An offer document is like a janam-kundli. It is the legal document

that binds the fund management company and the fund management team. The fund

management team has to manage the scheme in accordance with this document. This

is why details like the scheme’s objective, investment style and details of

where the money can be invested – are all part of this document. Apart from

this basic scheme related details, this document also gives details of the fund

management company as well as its promoters, which includes their financial

details. This helps one assess the financial and technical strengths of those

who manage your money. One can also access information (including the past

track record) regarding other schemes managed by the same fund management team.

The service and operational details are also a must.

Since the single document was becoming too bulky with too much

information, SEBI made an investor friendly change – breaking the document in

two parts, viz., Scheme Information and Statement of Additional Information.

The former carries details regarding the scheme one is considering, whereas the

latter details information regarding the fund management company and other

general details.

An investor is required to have read the offer document before

investing in the scheme. Please follow this advice as it is always in your

benefit to “look before you leap”.

Happy investing

- Amit Trivedi

Saturday, December 10, 2016

Wednesday, December 7, 2016

Are you ready to start on your own?

Be ready with a financial kitty for at least a couple of years. Here's some help on how to proceed

Click on this link to read further ...

(From archives)

Monday, December 5, 2016

Chitralekha - Birla Sun Life Mutual Fund Conclave yesterday (4th Dec, 2016) at Ahmedabad

What a response to this wonderful event. Thank you Ahmedabad. There were more than 250 people present on a Sunday morning to attend this function. Chitralekha had to close further registrations as the hall was already jam packed.

Fantastic audience. People listened to the speakers for over two hours and then there were many questions.

Thank you Ahmedabad once again. Thanks to Chitralekha and Birla Sun Life as well.

What you need to invst in equity markets - well, apart from money, time and knowledge ...

Below is the link to one of my old articles - published in Mumbai Samachar

http://www.bombaysamachar.com/frmStoryShow.aspx?sNo=29199

The English translation is as under:

Amit has authored a book "Riding The Roller Coaster - Lessons from financial market cycles we repeatedly forget. The book is available in two languages - English and Gujarati.

http://www.bombaysamachar.com/frmStoryShow.aspx?sNo=29199

The English translation is as under:

Mental fitness

Last week when

the Sensex made a two-year low, I received a sarcastic SMS from a friend: “New

SEBI rule from today: If you want to trade in stock markets or the derivatives

markets, additional documents must be submitted along with your PAN card and

KYC documents. These new documents include cardiograph, your blood pressure

readings and fitness certificate from a doctor.”

This conveys the

amount of stress that the stock market movements can cause to common men. Money has a profound impact on our mental

state.

I have always

wondered: I thought we invest our money to get peace of mind, but one has seen

many losing the peace of mind after investing. In fact, there have been cases

of suicide linked to losses incurred in the stock and derivatives markets. This

is very disturbing. Why should someone get into something that leads to such a

tragic end?

Does it mean

stock markets are bad? No, not really. It is like railway tracks. There have

been many cases of people losing lives while crossing railway tracks instead of

using the foot over bridge. Does it mean railway tracks are bad?

In majority of

such cases, the mechanism – be it stock markets or railway tracks – are made

for certain purpose. If one misuses the system, one should be ready to pay for

the consequences.

The other day,

one gentleman was talking to his friends about the stock markets and compared

the stock market with a casino. Very often, such phrases are used only because

there are some misunderstandings prevailing about the stock markets.

So let us

understand what exactly is the function of the stock market. As the name

suggests, it is a marketplace where buyers and sellers meet and exchange their

stocks or money. The stock market’s function is to provide a platform where

such transactions happen smoothly and very efficiently, at the same time

keeping the transaction costs as low as possible. Once such a platform is

available, the stock market is neutral. It does not know or care how one uses

this facility. It is available for the transactions.

Whether someone

buys it cheap or costly; whether someone sells it cheap or costly – the market

is neutral. It does not care at what price the transaction happens since it

allows each individual to take a decision to buy or sell at the prevailing price.

The transaction price is arrived at jointly by all the participants and is a

function of the demand-supply situation. The market does not determine the

transaction price.

The demand-supply

situation is a function of the information processed by the various buyers and

sellers. This is where the responsibility of proper assessment of information

lies with the person who transacts.

The stock market

provides a platform for the transaction and ensures that the cost of

transaction remains low.

One would be

better off treating the market only as a market – a place for carrying out the

transactions. Why one is selling or buying depends on an individual’s view on

the particular security.

We come back to

the initial paragraphs. If we understand the function of the market, it means

that the responsibility of the decision and its consequences lies only with us.

Taking these decisions requires mental toughness since at any time, there will

be people who have different views – some optimistic and some pessimistic. The

success in investing comes when one can take decisions with a calm state of

mind. To get a better perspective, please read the story of “Mr. Market” from

the book “Intelligent Investor” by Benjamin Graham.

Hence, I would

make a simple change in the SMS we spoke about in the first paragraph: One does

not need a cardiograph or blood pressure report; one needs a mental fitness

certificate. One needs to develop better abilities to take proper decisions to

succeed in the world of investing.

Happy investing!

Amit Trivedi

The author runs Karmayog

Knowledge Academy. The views expressed are his personal views. He can be

reached at amit@karmayog-knowledge.com.

Amit has authored a book "Riding The Roller Coaster - Lessons from financial market cycles we repeatedly forget. The book is available in two languages - English and Gujarati.

Sunday, December 4, 2016

Chitralekha presents Birla Sun Life mutual fund conclave

Venue: The Fern Hotel, Near Sola Overbridge, S G Highway, Ahmedabad

Time: Today at 10:30 AM to 1:00 PM

Monday, November 28, 2016

Why so many financial advisors and mutual fund distributors consider SIP as the best investment strategy?

When you talk to most mutual fund distributors

or financial advisors, you are most likely to come across one common

recommendation: start an SIP in a mutual fund scheme. Why do they so commonly

recommend this? Is SIP so good?

Click here to read the article as appeared in Mid-day Gujarati edition today ...

The English translation of the article is as under:

Click here to read the article as appeared in Mid-day Gujarati edition today ...

The English translation of the article is as under:

Why so many financial advisors and mutual fund distributors consider

SIP as the best investment strategy?

When you talk to most mutual fund distributors or financial

advisors, you are most likely to come across one common recommendation: start an

SIP in a mutual fund scheme. Why do they so commonly recommend this? Is SIP so

good?

Well, there are many arguments and counterarguments regarding the

merits of SIP. Some tend to indicate that investment through SIP may result

into higher returns as compared to lump sum investing and there are arguments

against this point. According to me, it is a fruitless exercise to try and

figure out which strategy would result into higher returns. It is not the rate

of return, but the amount accumulated for a goal that matters to an investor.

Given this, the discussion must shift to the amount required for the

goal and the time available for such accumulation. With this information in

hand, one has to plan to ensure enough amount is available at the time of the

requirement.

There are three approaches that one may adopt:

1.

Investing lump sum

2.

Investing small amounts on a

regular basis

3.

A combination of the above two

As we know, most of us often do not have large lump sum amounts

available for investment and that most of us earn, spend and save on a regular

basis. Due to this situation, regular investing becomes a better option, which

helps us channelize our regular savings into productive investments.

SIP is not about earning higher returns, but about getting into a

discipline of investing on a regular basis. It is this discipline that helps us

accumulate large sums over long periods. Remember the old saying,

Every drop makes an ocean

Small amounts invested over a period have the power to help one

reach one’s financial goals. This discipline is similar to the advice most

seasoned cricketers give young batsmen – keep taking one and two runs and don’t

rely heavily on the fours and sixes, keep rotating the strike. These runs add

up to many over the course of a match.

SIP allows you to buy a diversified portfolio through investing

small amounts on a regular basis. We have already seen the benefit of

diversification earlier. Add to that the other benefit offered by SIP – Rupee

cost averaging, which reduces the cost of buying the units. If you keep your

money invested for long periods, the power of compounding sets in, helping you

create a corpus enough to take care of your financial goals and your financial

future.

All the best! Save regularly, in a disciplined way through an SIP.

-

Amit Trivedi

Saturday, November 19, 2016

Cycle is the destiny

More than two decades of professional experience in capital markets.

As a trainer, trained more than 50,000 participants through 940

workshops (for mutual fund distributors, CFPs and regulators; as well as

for investors) across 98 different locations across the country.

Author of a book “Riding The Roller Coaster – Lessons From Financial

Market Cycles We Repeatedly Forget”, published by TV18 Broadcast Ltd, a

CNBC group company. Amit Trivedi writes about the eternal truth in this article.

Click here to read the article.

Click here to read the article.

Monday, November 14, 2016

PPF or debt mutual funds?

Now that the interest rate in PPF has come down and with the debt funds offering double digit returns, should one shift from PPF to debt mutual funds?

Click here to get the answer.

The English translation of the article is as under:

Click here to get the answer.

The English translation of the article is as under:

“Should I continue to invest in PPF at reduced interest rates or

invest in debt funds to earn between 9% to 12%?” Asked someone recently.

Looking at the question, it seemed he is a keen follower of the

financial markets. He was aware of the interest rates on PPF, which have been

recently lowered as well as the returns generated by various categories of debt

funds.

However, there is a small observation on what he observed. He was

referring to what interest rate would be earned in future on the investments in

PPF, the debt fund returns were those generated in the past. Aren’t high past

returns sustainable? Aren’t professional fund managers supposed to generate

high returns? Well, in order to get answers to these questions, it is important

to understand the reason why past returns are so high.

As of November 7th 2016, the returns generated by various

categories debt funds are as under:

|

Fund category

|

1 year return (%)

|

|

Debt: Gilt Medium

& Long Term

|

12.26

|

|

Debt: Dynamic Bond

|

10.85

|

|

Debt: Income

|

10.20

|

|

Debt: Credit

Opportunities

|

10.18

|

|

Debt: Short Term

|

9.33

|

Data as on Nov 07, 2016

As you can see, certain categories of debt funds have delivered

handsome returns given that the interest rates last year were below 10% in bank

deposits as well as Government Securities. So what caused the debt funds to

deliver such returns?

In the last one year, there was one factor that positively impacted

the investment returns – drop in interest rates. You may recall that we had

covered the impact of interest rate changes on debt securities and hence on

debt funds.

Interest rates and bond prices have an inverse relationship, i.e.

when the interest rates drop, bond prices rise and vice versa. When the bond

prices rise, the NAV of debt funds would also go up.

Now that is one of the components that contribute to debt fund

returns. The other component is the interest rates earned on the bonds or

debentures that fund has bought.

Let us take an example:

Say a mutual fund invested in the debenture of a company. The

debenture was available for purchase for Rs. 1,000 and it carried interest rate

of 9% p.a. After a year, similar debentures available in the market were

offering interest of 8.5% p.a. The earlier bond looks more attractive due to

higher interest rate. It is this increased attractiveness that results in rise

in price.

The bond fund would have gained from two things, (1) the 9% interest

earned on the bond, and (2) the rise in market price of the bond.

However, the moment the price goes up, the future earnings are now

adjusted in line with the new interest rates, i.e. from now onwards, the

earnings would be at the rate of 8.5% p.a.

In other terms, the future earnings gap between 9% and 8.5% has been

adjusted in the current price of the bond giving a capital gain.

With such an adjustment already completed, the future returns would

be a function of (1) current interest rates, and (2) any capital gain or loss

on account of change in interest rates in future.

In the above example, the interest rates reduced giving rise to bond

prices. If the interest rates in economy move up, the prices of bonds would go

down.

For the bond funds to deliver such high returns as the past one year,

the interest rates in the economy must drop further. Now that is something I

cannot predict.

Keep your expectations low. The past returns may not be sustained in

future. After having low expectations, if you get higher returns, enjoy.

At the same time, let us not forget some major benefits offered by

debt mutual funds. These are:

·

Diversified portfolio

·

Professional management of the

funds

·

Easy and convenient liquidity

·

Flexibility to invest in the

same folio

·

Flexibility to redeem full or

part of the investments

·

Tax efficiency

It is not just the investment returns, there are many other factors

that one must keep in mind before taking an investment decision.

- Amit Trivedi

Tuesday, November 8, 2016

Monday, November 7, 2016

Transcript of today's chat on www.moneycontrol.com

Click on the link below to read the transcript of chat on www.moneycontrol.com today:

Equity investments simplified

Equity investments simplified

Today @ 4 PM: Get answers to your questions on mutual funds

Karmayog Knowledge Academy: Get answers to your questions on mutual funds: Do you have questions regarding mutual funds? Get answers during the live chat on www.moneycontrol.com on 7th November, 2016 at 4:00 PM to ...

How active is your equity fund?

How active is your equity fund, really? Is there a difference between an active fund and a passive fund? Are all actively managed funds really very actively managed? How do you know?

Click here to read further.

Click here to read further.

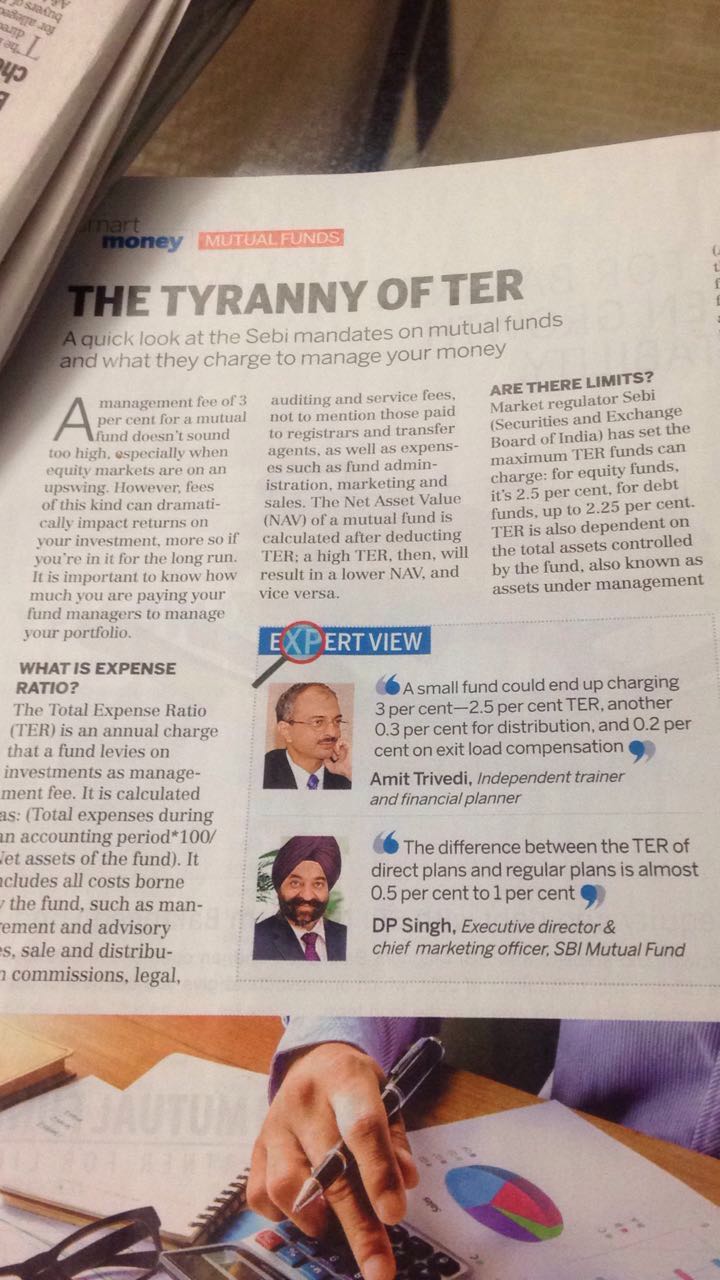

Saturday, November 5, 2016

Quoted in India Today

In a story related to the TER on mutual funds, my quote was taken by India Today.

Here is the photo of the relevant page

Here is the photo of the relevant page

Thursday, November 3, 2016

Get answers to your questions on mutual funds

Do you have questions regarding mutual funds? Get answers during the live chat on www.moneycontrol.com on 7th November, 2016 at 4:00 PM to 4:30 PM

Tuesday, October 25, 2016

Build wealth through mutual funds - chat transcript

Transcript of my chat today on www.moneycontrol.com

http://www.moneycontrol.com/news/mgmtinterviews/chats/detail_new.php?chatid=24&source=mym

http://www.moneycontrol.com/news/mgmtinterviews/chats/detail_new.php?chatid=24&source=mym

Master Your Money - live chat

I will be answering questions on live chat on www.moneycontrol.com in the Master Your Money segment today between 3:00 to 3:30 PM

Monday, October 24, 2016

A good investment option amidst volatility

We looked at various asset allocation schemes last time. This time, we will discuss a variation of these schemes - dynamic asset allocation schemes.

Click on the link here to read further.

____________________________________________________________________________________

The English translation is as under:

Click on the link here to read further.

____________________________________________________________________________________

The English translation is as under:

Last time, we covered asset allocation funds. This time we will look

at a variant of the same, known as “dynamic asset allocation” funds. While we

discussed about investing in multiple asset categories, the focus of the

discussion was about maintaining certain proportion in each of the two or three

asset categories.

However, periodically, when one asset category becomes costly, does

it make sense to reduce the allocation? Similarly, should one increase the

allocation in the asset that has become cheaper? There is a school of thought

that suggests, “Yes, we should”.

Mutual fund companies have come up with schemes that work on such

principles. These schemes invest in more than one asset categories – in most

cases these invest in two assets. Most such schemes allocate money between

equity and debt.

The allocation between equity and debt is altered periodically. In

order to determine the allocation to the two asset categories, there are two

approaches:

1.

The fund manager alters the

allocation based on his/her views on the two asset categories.

2.

The allocation would change on

the basis of some pre-decided formula.

In the first case, when the fund manager is bearish on equity

market, the scheme would reduce equity exposure. However, when one is bullish

about equity, the allocation would go up.

In the latter, most often, valuation determines how much should be

allocated where. The allocation would be reduced from (or increased in) the

asset that has become costly (cheaper) as indicated by certain valuation

parameters. However, some of the schemes only look at valuation of equity.

There is at least one scheme that compares the valuation of equity and debt and

changes the allocation accordingly.

The valuation parameters:

For the purpose of evaluating equity valuation, most consider the

P/E ratio or the P/BV ratio. Both these ratios are popular indicators of

valuation. As a thumb rule, it is believed that higher the number, costlier the

market (or a sector or a stock). Fund schemes follow a certain pre-defined

pattern through which the allocation in equity is reduced step-by-step when the

valuation goes up and increased when the valuation goes down.

In one case, the scheme’s allocation is altered based on the gap

between the yield on Government Security with 10-year maturity and the

“earnings yield” for equity. The earnings yield is the inverse of P/E ratio.

These are schemes designed to reduce short-term fluctuations in the

scheme’s NAV. At the same time, such schemes are expected to deliver at least

as much as a fund that evenly allocated money between equity and debt.

Very often, investors have compared such schemes to pure equity

funds. That is a mistake. Given that these schemes invest at least some

proportion and often a large chunk in debt securities, it would be improper to

compare these with pure equity funds.

Should an investor consider investing in such schemes? Well, that

entirely depends on whether the investor needs such a scheme in the first

place. Having said that, one may consider such a scheme with an expectation of

reduced price fluctuations compared to a hybrid scheme that does not change the

allocation.

It’s a good category to explore for investors. However, a deeper

analysis is warranted since the alternatives can have significant differences

among them.

-

Amit Trivedi

The

author runs Karmayog Knowledge Academy. Recently, Amit has authored a book

titled “Riding the Roller Coaster –

Lessons from Financial Market Cycles We Repeatedly Forget”. The views

expressed are his personal opinions.

Monday, October 17, 2016

Another high on the roller coaster ride

Gujarati edition of my book "Riding The Roller Coaster - Lessons from financial market cycles we repeatedly forget" is available for pre-order now on www.amazon.in

See the details below:

Subscribe to:

Posts (Atom)